Solutions

Securely accept, manage, and make payments through one point of integration

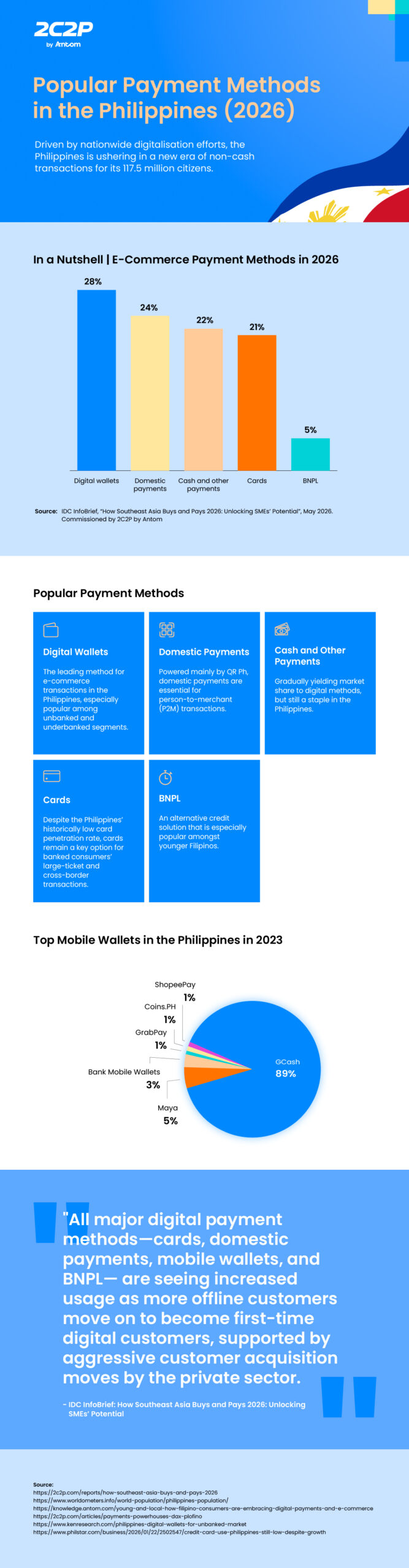

The Philippines has the second-largest population in Southeast Asia, at 117.5 million people. While cash used to dominate the country’s payment landscape, the Philippines has made significant progress in driving widespread digital payment adoption.

Traditionally one of the cash-heaviest nations in Southeast Asia, the Philippines has since experienced rapid growth in its digital payment landscape.

According to 2C2P’s commissioned IDC InfoBrief 2026, the country recorded a total e-commerce volume of US$20 billion in 2026, with digital payments like digital wallets and real-time domestic payments constituting an overwhelming 73%. This stands in stark contrast to cash and other alternative payments, which take up just 27% of the pie.

Recent data from the Bangko Sentral ng Pilipinas (BSP)’s 2024 Status of Digital Payments in the Philippines report corroborates these figures. The country’s central bank reports that digital retail payments accounted for 57% of total retail payment volume, tracking ahead of the Philippine Development Plan (PDP) 2023-2028’s targets of 52-54%.

Underpinning this shift is the BSP’s National Retail Payment System (NRPS), a policy and regulatory framework that built critical real-time payment rails like InstaPay and PESONet to facilitate digital transactions in the Philippines.

Alongside the widespread adoption of the national QR Ph standard, these factors have gone a long way in ensuring that many of the Philippines’ residents have reliable, accessible methods to transact digitally.

In this article, we explore the Philippines’ most popular payment methods, including:

Digital wallets take the lead in the Philippines, accounting for an estimated 28% (US$ 5.6 billion) of total e-commerce transactions in 2026. This share is projected to rise to 31% (US$ 8.68 billion) by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

As the undisputed engine of e-commerce in the Philippines, digital wallets have transcended basic payments to become comprehensive digital financial hubs for Filipinos.

While COVID-19 is credited for catalysing the hyper-growth of digital wallets, the apps themselves have continued to aggressively expand their product offerings to include micro-lending, savings, investments, and remittance. This makes digital wallets perfect for reaching the unbanked and underbanked segments, granting them access to essential financial services without needing to open a formal bank account.

Consequently, this means that merchants must have digital wallets available at checkout to maximise consumer conversions in the Philippines.

Of these digital wallets, GCash stands as the most crucial option that merchants must account for in the market, as it commands a staggering 89% of the domestic wallet share. According to Antom’s analysis on Filipinos’ digital payment and e-commerce payments, these are the Philippines’ top digital wallets in 2023:

GCash enjoyed a momentous first-mover advantage during COVID-19, with many Filipinos turning to its simple mobile payment service to facilitate payments during the pandemic. It has since transformed into a household superapp in the Philippines, recording over 94 million users in 2025 alone.

As Martha Sazon, President and CEO of Mynt, GCash’s parent company, shared,

“Digitalisation has enhanced [GCash’s] convenience and access to opportunities, transforming [it] from a simple wallet into a personal digital life hack.”

Domestic payments do not lag far behind digital wallets, accounting for an estimated 24% (US$ 4.8 billion) of total e-commerce transactions in 2026. They are expected to increase their share to 26% (US$ 7.28 billion) by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

Driven by the Bangko Sentral ng Pilipinas (BSP) and the National Retail Payment System, domestic retail payments in the Philippines are primarily powered by QR Ph and InstaPay.

While the country’s national framework includes two main real-time payment systems—InstaPay and PESONet—PESONet is designed for higher-value, batch electronic fund transfers like corporate bulk payments and payroll, rather than everyday consumer transactions.

For retail payments, QR Ph takes center stage. Built directly on the InstaPay rail, QR Ph facilitates fast, low-value real-time transfers, giving Filipino consumers a unified, interoperable standard that prioritises speed and convenience across different banks and e-wallets.

Although InstaPay and PESONet collectively recorded a total transaction value of PHP 7.69 trillion (US$ 126.6 billion) as of March 2026 (a 45.32% jump from Q1 2025), it is the widespread adoption of QR Ph and its underlying InstaPay infrastructure that drives the consumer payment experience.

Further supporting InstaPay and PESONet is the Philippines’ national QR Ph standard. First implemented in 2023, the QR Ph standard simplifies person-to-merchant (P2M) transactions by enabling merchants to simply display a single interoperable QR code that accepts all digital payments. This includes InstaPay, participating banking apps, and wallets like GCash, in turn drastically lowering the barrier to entry for digital payment acceptance.

This is why the number of merchants accepting QR Ph increased by 148.7% year-on-year in 2024, offering consumers an easy and efficient way to pay for their e-commerce purchases in real time.

Looking ahead, the Philippines is actively exploring cross-border linkages with other real-time payment schemes to improve payment interoperability within Southeast Asia. One such linkage is between the Philippines and Singapore, for which the Monetary Authority of Singapore (MAS) and BSP inked an agreement in 2021.

Cash and other payments rank third at an estimated 22% (US$ 4.4 billion) of e-commerce transactions in 2026. This figure is expected to decline sharply to just 15% (US$ 4.2 billion) by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

Looking at prevalent attitudes towards payments in the Philippines, the continued preference for cash is not because Filipinos are unreceptive to digital payment methods. Rather, they view cash as a crucial psychological safety net that digital payments are still seemingly unable to provide.

In fact, 2024 data reveal that at least 85% of Filipinos utilised cash-on-delivery to pay for their e-commerce orders. Surveyed respondents indicated that they had lingering trust issues regarding product quality, high delivery fees, and, most importantly, cybersecurity and privacy risks. At least 53% of surveyed respondents felt comfortable sharing their personal details for online deliveries, while 31% saw online shopping as risky.

Such concerns about cybersecurity risks are not lost on the central bank, Bangko Sentral ng Pilipinas (BSP), recognising that they are a huge barrier to more widespread adoption of digital payments in the Philippines.

As part of the plan to build public trust in digital payments, BSP Deputy Governor Mamerto Tangonan has committed to strengthening anti-fraud safeguards. BSP had also previously enacted Republic Act No. 12010 or the Anti-Financial Account Scamming Act in 2024, signalling its commitment to combating financial scams, protecting consumers, and strengthening trust in the financial system.

Cards account for a modest estimate of 21% (US$ 4.2 billion) of total e-commerce transactions in 2026, according to 2C2P’s commissioned IDC InfoBrief 2026. According to another study, cards primarily drive the country’s highly active cross-border e-commerce sector, by accounting for a substantial 28% of total online sales in 2024. Primarily, they use cards to pay for international travel bookings, digital subscriptions, and international orders.

Cards are widely used by the banked middle-to-upper-class population. On the whole, however, this segment covers a small fraction of the total Philippine population, which is reflected in the country’s overall historically low card penetration rates. This is especially true for credit cards: as of Q4 2025, the Credit Card Association of the Philippines (CCAP) recorded 18.5 million outstanding credit cards issued, a relatively low figure when weighed against the country’s 70-million-strong adult population.

However, this looks set to change with the Philippines’ renewed commitment to increase card adoption. As CCAP executive director Alex Ilagan shared with The Philippine Star, the country has made inroads in dismantling barriers that once discouraged Filipinos from applying for credit cards, including the absence of formal identification and credit records. To further demonstrate this commitment, he cited the Credit Information Corp., the country’s national credit registry, which has 60 million unique data records, alongside the rollout of the national ID system.

Consequent to these efforts to expand card adoption, 2C2P’s commissioned IDC InfoBrief 2026 projects that cards will grow to make up 23% (US$ 6.44 billion) of total e-commerce transactions by 2029.

In anticipation of the eventual growth of cards in the Philippines, merchants should look towards implementing standardised, frictionless solutions like Click to Pay.

Buy Now, Pay Later (BNPL) comes in last at an estimated 5% (US$ 1 billion) of total e-commerce transactions in 2026, projected to grow to 6% (US$ 1.68 billion) by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

Although BNPL holds a smaller percentage of overall e-commerce volume, it remains an important payment method in the Philippines. Given the country’s low card penetration rate, alongside a still-sizable unbanked and underbanked population, BNPL provides a low-barrier, flexible alternative for financing mid-to-high-tier purchases like smartphones and home appliances.

Similar to its other Southeast Asian counterparts, the Philippines’ BNPL growth is predominantly driven by younger consumers, with millennials and Gen Z tending to be more receptive towards its card-free model to break up their purchases into more manageable instalments.

At present, the top three BNPL companies in the Philippines are Billease, SPayLater (integrated within Shopee), and Home Credit.

Other major digital wallets like GCash and Maya have also begun rolling out their own native, integrated BNPL services, which only means that adoption will continue to skyrocket over time. Merchants should thus ensure they offer BNPL as a payment option to leverage this upcoming trend.

Digital payments are on the uptick in the Philippines. The Philippine market seems set to continue migrating toward a cash-lite economy, as the government and local banks ramp up efforts to drive digital payment adoption across all segments of society.

Technologies such as softPOS will provide merchants with flexible, cost-effective ways to manage digital payments without dedicated terminal hardware. At the consumer level, agentic AI will refine e-commerce interactions, deploying autonomous bots to simplify the payment process and even carry out transactions on behalf of users. And as the Philippine payment ecosystem digitalises, securing these payment flows will become increasingly essential.

2C2P empowers merchants to stay ahead of the curve by actively exploring and implementing these new technologies, giving businesses the secure, compliant solutions needed to scale reliably.

Learn more about the top payment methods around the world. Check out the other articles in our Popular Payment Methods series: