Solutions

Securely accept, manage, and make payments through one point of integration

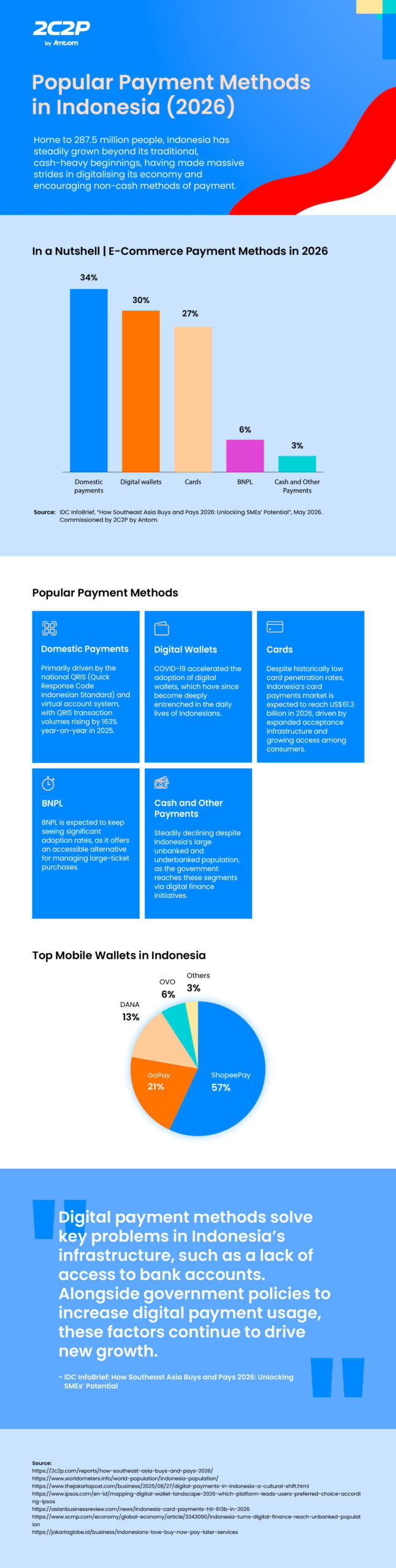

Boasting the largest e-commerce market in Southeast Asia, Indonesia’s digital payments sector naturally operates at a significant scale. According to estimates by 2C2P’s commissioned IDC InfoBrief 2026, Indonesia’s e-commerce market is expected to reach US$94 billion in 2026, of which at least 97% is projected to be transacted through digital payment methods such as digital wallets and domestic payments. This figure is expected to expand to US$139 billion by 2029.

The burgeoning growth of digital payments in Indonesia is not unprecedented. Joint efforts by the government and the country’s central bank, Bank Indonesia, have led to the rapid implementation of the Quick Response Code Indonesian Standard (QRIS). The standard has played an instrumental role in bringing interoperability to Indonesia’s diverse payments market, bridging various banks and digital wallets, and giving Indonesian merchants more options for simplifying payment acceptance.

In this article, we explore Indonesia’s most popular payment methods, including:

Domestic payments take the lead in Indonesia, accounting for an estimated 34% (US$31.96 billion) of e-commerce transactions in 2026. Their growth is expected to remain strong and contribute 36% of total e-commerce transaction value (US$50.4 billion) by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

The QRIS (Quick Response Code Indonesian Standard) and virtual account systems are key drivers of domestic payments in Indonesia. This is demonstrated by official figures from Bank Indonesia in July 2025, which revealed that QRIS transaction volume had risen by 163% year-on-year (YOY).

QRIS was launched by Bank Indonesia in 2019, intended to facilitate real-time, near-instant interbank transfers and person-to-merchant (P2M) payments. As its name suggests, QRIS mandates all payment providers to use a single, standardised QR code format for payments.

This alone is revolutionary for merchants, as QRIS enables them to simply display a single QRIS code instead of managing multiple QR code formats from different payment channels. Consumers can then scan and pay using their preferred digital wallet or banking app, ensuring maximum convenience and minimal checkout friction. QRIS has also been augmented with cross-border real-time payment capabilities, with linkages forged with Thailand, Singapore, Malaysia, and China.

As for virtual accounts, they provide consumers with a dynamically generated account number that is tied directly to a specific checkout session. This enables merchants to automatically identify and reconcile payments in real time, a stark contrast to the traditional method of requiring consumers to upload proof of payment. With their transactions often powered by BI-FAST, Bank Indonesia’s national retail payment infrastructure, virtual accounts facilitate fast and easy interbank transfer between consumers and merchants.

This creates a highly efficient, 24/7 payment ecosystem. Together, they ensure a seamless, cost-effective checkout experience that is critical for scaling operations within Southeast Asia’s rapid digital economy.

Looking ahead, Bank Indonesia has already pipelined several upgrades, including bank-to-digital-wallet interoperability, QRIS tap-to-pay via near-field communication (NFC), and smart transaction routing.

Digital wallets are a close second after domestic payments, accounting for an estimated 30% (US$28.2 billion) of e-commerce transactions in 2026, and expected to continue growing steadily to reach 31% (US$43.9 billion) by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

COVID-19 was a key driver of digital wallet adoption in Indonesia between 2019 and 2021, and its prevalence has continued well into 2026, with at least 96% of Indonesians using digital wallets in 2024.

Digital wallets have evidently become deeply entrenched in the daily lives of Indonesians, with the tech-savvy and mobile-first younger generations primarily driving their popularity. These younger generations are often credited with leapfrogging traditional desktop banking entirely to adopt mobile alternatives like digital wallets.

According to Ipsos Indonesia’s Mapping the Digital Wallet Landscape in 2026 report, the top digital wallets used for e-commerce in Indonesia are as follows:

In general, digital wallets that are integrated within larger superapp ecosystems experience higher usage. ShopeePay, for example, is intertwined with the broader Shopee e-commerce platform, enabling users to buy food and groceries, pay for digital products and bills, and even top up games within one consolidated app.

The same report by Ipsos Indonesia reveals that the country’s Gen Z population is the largest driver of digital wallet usage, broken down into the following key segments:

For merchants, this means that supporting Indonesia’s most popular digital wallets taps directly into a captive audience with ready funds, reducing friction at the point of sale.

Cards are almost neck-to-neck with digital wallets, contributing an estimated 27% (US$25.38 billion) of e-commerce transaction volume in 2026. While the overall e-commerce transaction volume for cards is expected to rise to US$36.14 billion by 2029, its share of total e-commerce volume is projected to dip slightly to 26%, according to 2C2P’s commissioned IDC InfoBrief 2026.

Indonesia’s card penetration rate has historically been low, with just 6-7% of the country’s population owning credit cards in 2025. This is largely due to two key reasons:

Despite these factors, Indonesia’s card payments market is expected to reach US$61.3 billion in 2026, the result of expanded payment acceptance infrastructure and growing familiarity with digital payments.

Notably, debit cards accounted for 53% of total card payments in 2025, while credit and charge cards made up the remaining 47%. The overall growth of cards can be attributed to several factors, such as:

Buy Now, Pay Later (BNPL) are expected to contribute an estimated 6% (US$5.64 billion) of e-commerce transactions in 2026. By 2029, BNPL is also projected to see a modest 1% growth in Indonesia to reach 7% of all e-commerce transaction volume (US$9.73 billion), according to 2C2P’s commissioned IDC InfoBrief 2026.

Once a nascent payment method that was not well understood, BNPL has since become a prominent and rapidly scaling feature in Indonesian e-commerce. In 2025, data from the Financial Services Authority (OJK) revealed that banking-based BNPL account numbers rose from 30.99 million in October to 31.47 million in November, with outstanding BNPL balances reaching a combined volume of US$2.2 billion. Indonesian banks have also increasingly launched their own BNPL schemes, resulting in bank-issued paylater credit spiking to 21.8 trillion rupiah (US$1.3 billion) in November 2024, marking a 43% year-on-year increase.

This signals Indonesia’s growing adoption of BNPL, prompting OJK to increase its supervision of the payment method through Regulation No. 32/2025, which aims to mitigate defaults, lack of informational transparency, and also reduce operational and systemic risks inherent to digital financing platforms. In turn, this also indicates BNPL’s longevity in Indonesia, with an official government body regulating it to ensure it stays sustainable without compromising consumer safety.

Given Indonesia’s low card penetration rate, BNPL’s popularity is hardly surprising. It serves as a critical, inclusive credit alternative for the unbanked and underbanked populations, giving them an easy means to make installment-based payments with little to no interest. BNPL services are often integrated natively into superapp platforms like Tokopedia and Shopee, enabling users to activate installment plans with just a few taps. This immediate access to credit is a powerful driver for consumer spending, effectively raising the ceiling on average order values for local merchants.

Cash and other payments come up last at an estimated 3% (US$2.82 billion) of e-commerce transactions in 2026, and are expected to continue declining to zero by 2029, according to 2C2P’s commissioned IDC InfoBrief 2026.

The increasing unpopularity of cash and other alternatives like over-the-counter (OTC) payments is especially interesting, given that Indonesia continues to record a massive unbanked population of 97.74 million, or 47% of the adult population, in 2024. This places Indonesia at fourth globally in terms of unbanked individuals.

After all, paper money dominated Indonesia not so long ago, with convenience store networks like Indomaret and Alfamart allowing customers to pay for online orders with physical cash at local stores. But the tides have shifted, as Indonesia has ramped up its efforts to reach unbanked and underbanked populations via digital finance.

This is why cash and other alternatives are expected to be completely phased out by 2029, as cash-reliant consumer segments residing outside major metropolitan hubs are gradually converted to digital-first methods in line with Indonesia’s wider vision.

The digitalisation of Indonesia’s payment ecosystem is proceeding at a rapid pace.

Looking ahead, the deployment of technology like softPOS opens up more opportunities to further democratise payment acceptance in Indonesia, empowering merchants of all sizes to transform smartphones into secure, cashless transaction points. The rise of agentic AI will also introduce autonomous bots to the equation, introducing the possibility of greater AI involvement in everything from consumer checkouts to fraud monitoring.

However, navigating this future requires more than just acknowledging trends. Indonesia’s massive market, combined with its highly fragmented financial landscape, spans hundreds of local banks, e-wallets, and emerging credit solutions. Keeping up with these constantly shifting consumer preferences while integrating new technologies can be an immense operational burden.

This is where a payment partner like 2C2P becomes crucial. With 2C2P, merchants will be able to keep up with Indonesia’s sprawling ecosystem through a single, flexible integration. In turn, merchants are empowered to adapt to local preferences, deploy emerging payment methods, and focus on growth instead of getting mired in technical and operational complexity.

As digital transaction volumes surge across Indonesia, this growth must be built on trust. This is also where 2C2P comes in, helping merchants stay agile while providing the enterprise-grade infrastructure necessary to manage high transaction volumes without compromising on security. With strong security protocols, 2C2P gives businesses the power to confidently and securely step into Indonesia’s digital future.

Learn more about the top payment methods around Asia. Check out the other articles in our Popular Payment Methods series: